-

M&A

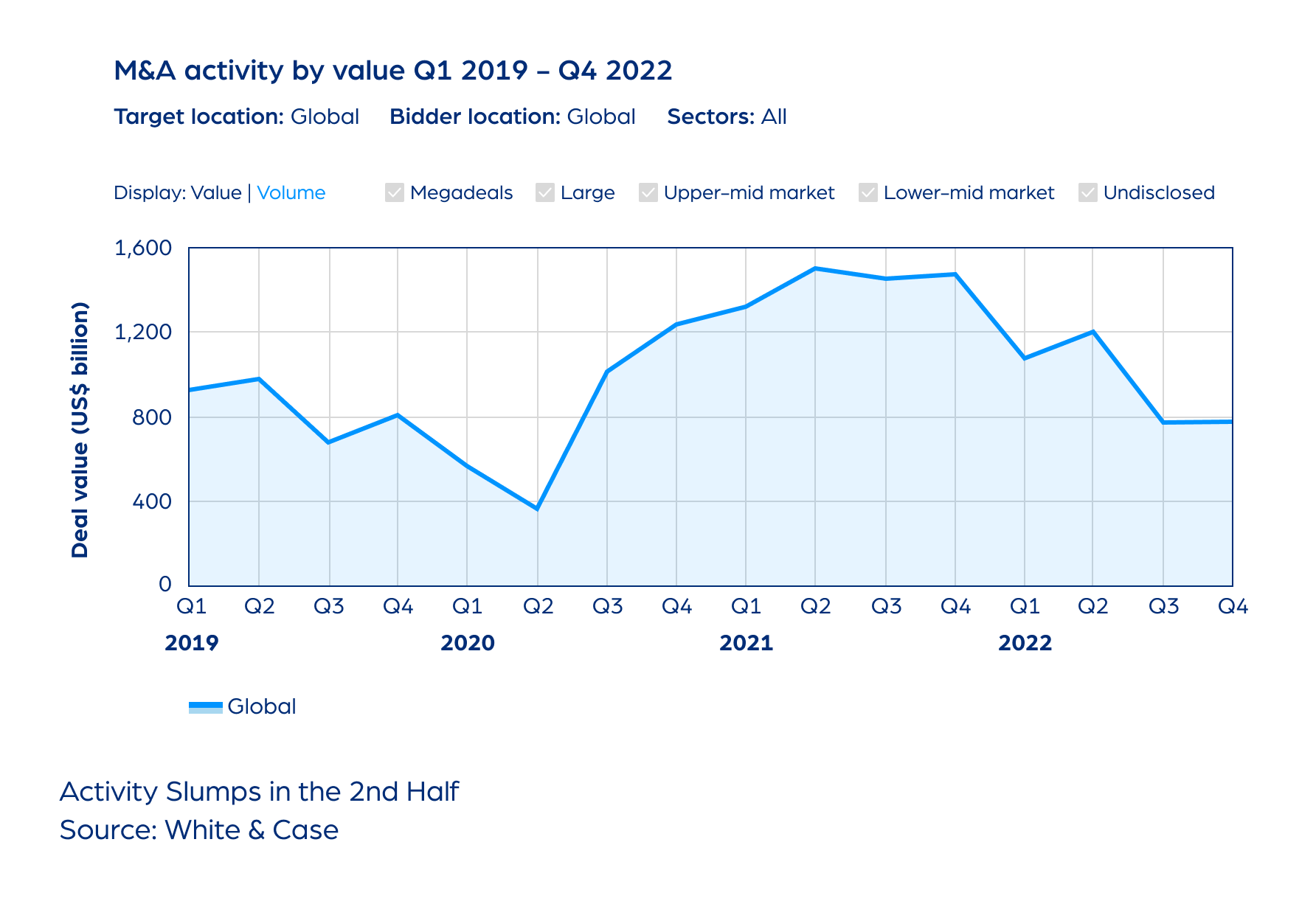

Q3 M&A Recap: Global Activity Sluggish, US Leads

-

Venture Capital

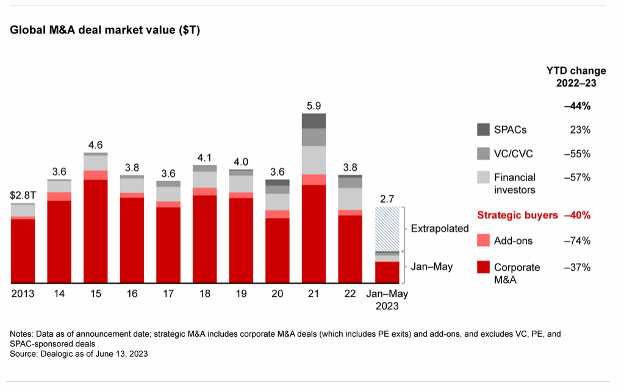

Private Equity 2023 Mid-Year Recap: A Tough First Half

-

Virtual Data Room

Revolutionizing Board Communications with Virtual Data Rooms

-

M&A

Q2 2023 Yields Cautious Optimism for M&A

-

M&A

Q1 M&A: Running Against the Wind

-

M&A

Q1 Life Sciences: Resilient in a Changing Landscape

-

IPO

IPOs plummet in 2022. What Comes Next?

-

M&A

2022: Tough Environment, Resilient Market

-

M&A

Earnouts: Seeking Safety in a Transaction

-

Fundraising

5 Common Fundraising Questions Answered

-

Startups

Corporate Repository: Rethinking the Way You Do Business

-

Audits

Simplify Your Audit With a Virtual Data Room

current_page_num+2: 3 -

Ready to Get Started?

Start your free trial of SecureDocs today. Your data room will be available immediately—no need to talk to a salesperson.